Sandro Sarukhanishvili is a qualified lawyer with a Doctor of Laws (LL.M.), specializing in civil and administrative law, big data, digital commerce and digital markets law. He has significant experience in banking, drafting legal documents, contract analysis and compliance. Sandro received his Master of Laws degree from Sulkhan-Saba Orbeliani University (2020-2022). Prior to that, he obtained his Bachelor of Laws degree from Tbilisi State University (TSU) in 2015-2019. Sandro studied on exchange at the University of Cadiz, Cadiz, Spain (2024-2025), LUMSA, Rome, Italy (2021-2022) and Vilnius University, Vilnius, Lithuania (2017-2018). Sandro's professional skills include legal research, problem solving, analytical thinking, and legal writing. He is proficient in Microsoft Office programs and legal databases. His strengths include detail-oriented, critical analysis, adaptability, organization, and communication skills.

4 articles • 2 categories

The text analyses a commercial bank's marketing campaign (a discount on tickets to a Kanye West concert) as a potential example of a dual strategy that simultaneously serves direct financial gain and the capitalization of consumer data.

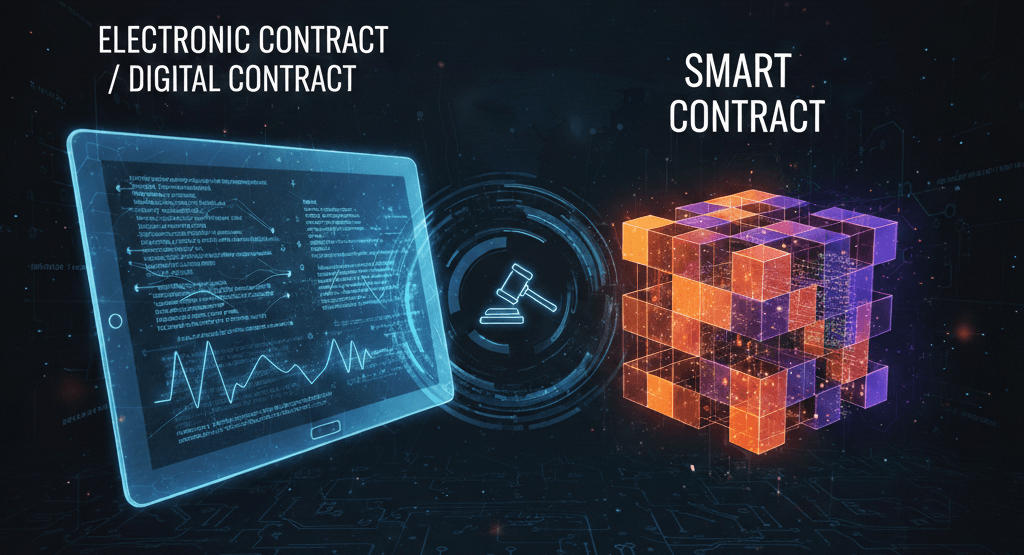

Digital contracts and smart contracts intersect across the following dimensions: Taxonomic Classification: A smart contract is categorized as a subset of an electronic contract. It functions similarly to a traditional agreement, though executed in a comprehensively digitized format. Legal Nature: Smart contracts, analogous to other digital contracts, are encompassed within the legal definition of an electronic document. For a smart contract to constitute a legally binding agreement, it must fulfill the fundamental prerequisites of contract formation and validity (e.g., mutual consent of the parties and adequate terms)—requirements that programming code alone cannot substitute. Functional Overlap: Within the processes of concluding and executing a digital contract, a smart contract may be implemented as a technological utility (for example, as an automated payment mechanism for recurring transactions).

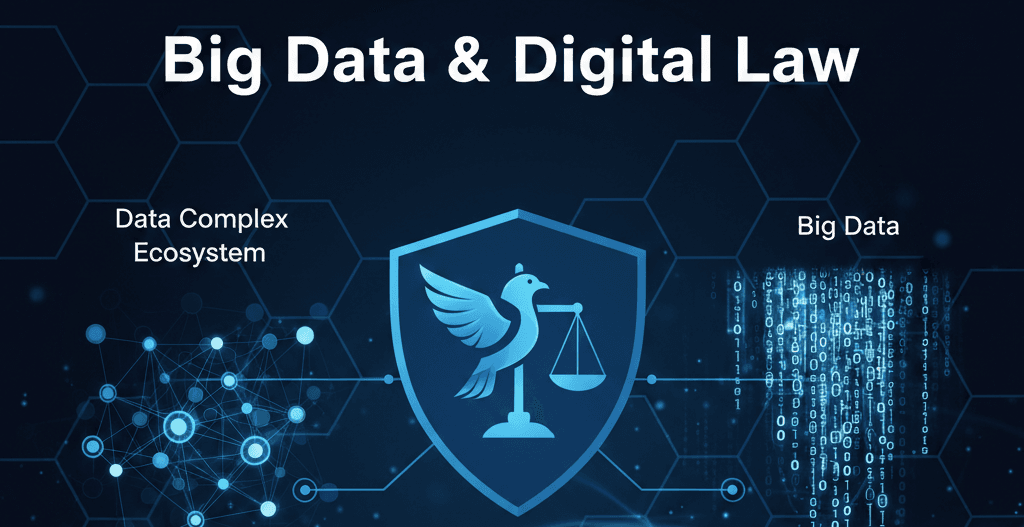

The legal regulation of the digital economy requires understanding the technological foundations driving the financial and business sectors. This analysis identifies four essential pillars for legal professionals: Big Data: Substantial volumes of heterogeneous digital data, facts, and unrestricted activities collected at high velocity. It is characterized by real-time processing through advanced analytical algorithms. Big Data Complex Ecosystem (BDCE): An IT infrastructure consisting of integrated systems for data collection, storage, and use. It unites data owners, cloud providers, and academic institutions into a unified infrastructure. Data Architecture: A component of the BDCE that defines how data is processed, stored, and integrated for organizational purposes. It serves as a conceptual model for data governance, lifecycle management, and security. FinTech and Big Personal Data: Financial Technology leverages Big Data, AI, and Distributed Ledger Technologies (DLT) for platform-based service delivery. This process generates "Big Personal Data"—personal information created or processed within these complex ecosystems.

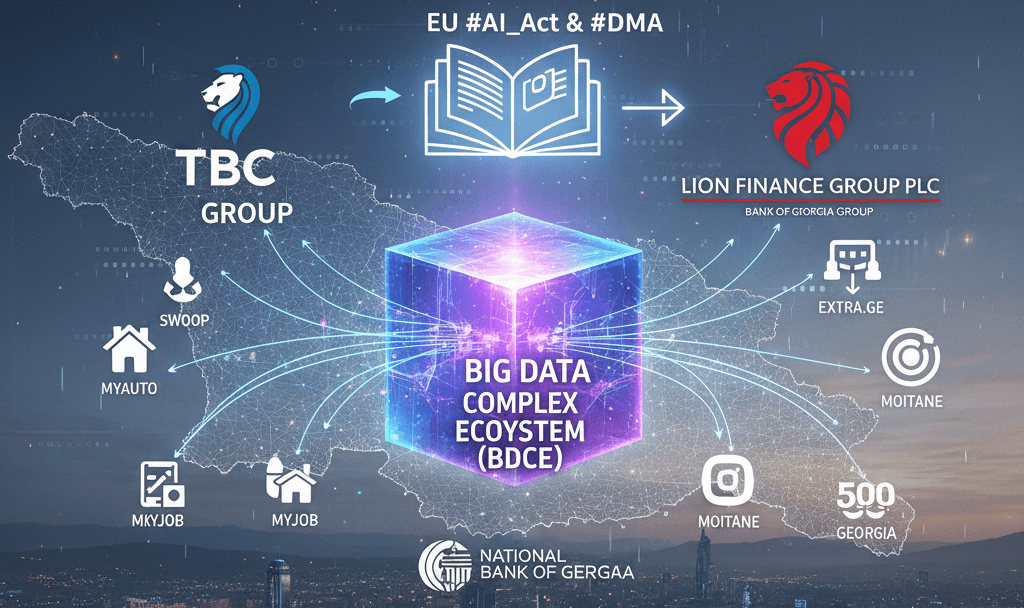

In today's fast-moving digital economy, the lines between where we bank and where we shop, work, and live are becoming increasingly blurred. In Georgia, this evolution has reached a critical tipping point as the nation's two largest financial giants—TBC Group and Lion Finance Group PLC (formerly Bank of Georgia Group)—have successfully built sprawling "digital ecosystems" that touch almost every aspect of a citizen's daily life. From buying a car on MyAuto to managing a small business with Optimo, these platforms are no longer just apps; they have become the "gatekeepers" of the Georgian digital marketplace. While this integration offers undeniable convenience, it raises a profound structural question for our market: What happens when the people who hold our money also hold all of our data?